We all encounter situations where our applications for loans, jobs, or apartments get rejected, and it can be disheartening. But did you know that there’s a legal requirement in place to ensure you are informed about the reasons for these rejections? It’s called the Fair Credit Reporting Act (FCRA) Adverse Action Notice. This article aims to provide you with a comprehensive understanding of what the FCRA Adverse Action Notice entails, why it is important, and how it protects your rights as a consumer. So, the next time you receive an adverse action notice, you can approach it with confidence and knowledge.

What is the FCRA Adverse Action Notice?

The FCRA Adverse Action Notice is a legal requirement under the Fair Credit Reporting Act (FCRA) that businesses must follow when taking adverse actions against consumers based on their credit reports. An adverse action refers to a negative decision, such as denying a credit application, increasing interest rates, or denying employment, which is influenced by the information found in a consumer’s credit report.

Definition and purpose of the FCRA Adverse Action Notice

The FCRA Adverse Action Notice serves as a notification to consumers about the unfavorable outcome resulting from an adverse action taken by a business. Its purpose is to ensure transparency and fairness, allowing consumers to understand the reasons behind the decision and providing them with an opportunity to review and correct any inaccurate information on their credit report.

Legal requirements for the FCRA Adverse Action Notice

The FCRA Adverse Action Notice is a legal requirement aimed at protecting consumers’ rights and promoting fair credit practices. It is covered under section 615(a) of the FCRA and enforced by various regulatory agencies such as the Consumer Financial Protection Bureau (CFPB) and the Federal Trade Commission (FTC). Businesses must comply with specific criteria when providing the notice to consumers.

Who is Required to Provide the FCRA Adverse Action Notice?

Businesses subject to the FCRA

The FCRA Adverse Action Notice requirement applies to a wide range of businesses that use credit reports to make decisions. This includes lenders, employers, landlords, insurance companies, utility providers, and other entities that use consumer credit information in their evaluation processes. Regardless of the type of business, if credit information forms the basis for an adverse decision, the FCRA Adverse Action Notice is mandatory.

Types of actions that trigger the requirement for an FCRA Adverse Action Notice

Any adverse action taken by a business, which is partially or wholly based on the information contained in a consumer’s credit report, triggers the obligation to provide an FCRA Adverse Action Notice. Common examples of adverse actions include denying credit applications, increasing interest rates, modifying credit terms, and denying employment or housing applications. It is vital for businesses to recognize when they are in a situation that requires them to provide the notice.

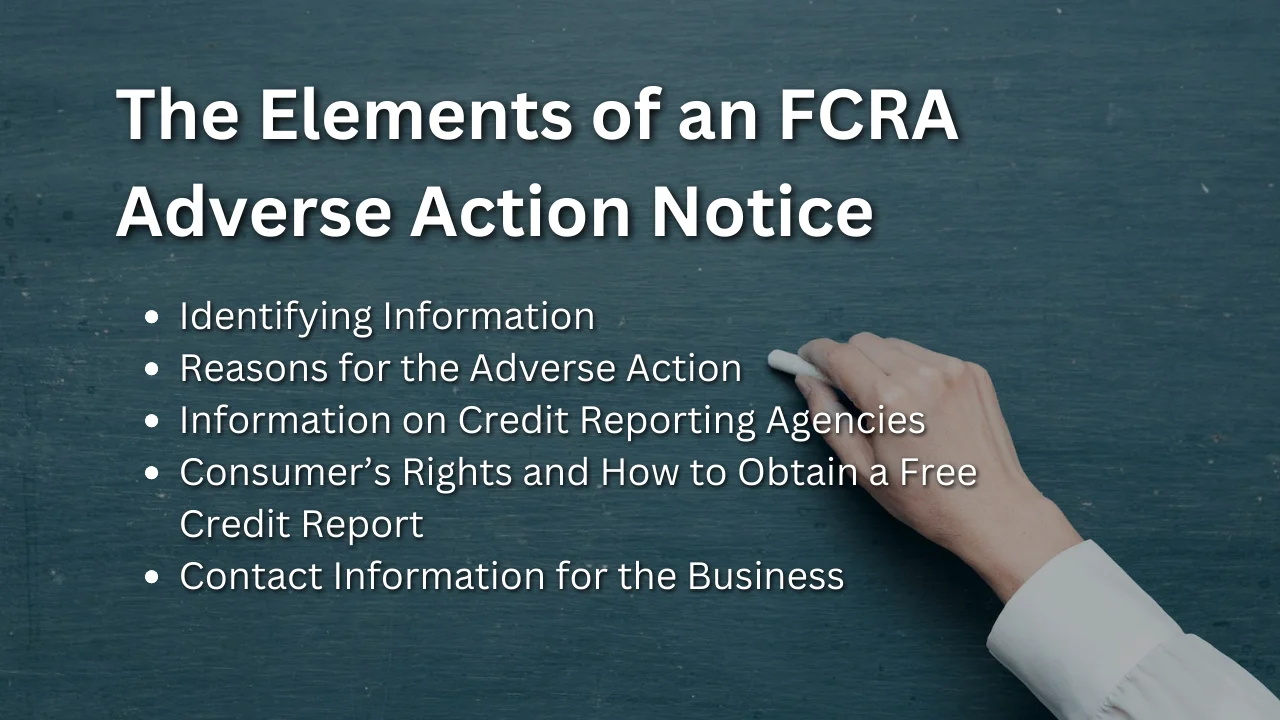

The Elements of an FCRA Adverse Action Notice

Identifying information

An FCRA Adverse Action Notice must contain the necessary identifying information to help consumers understand the specific adverse action being taken against them. This includes the name and address of the business, the date the notice was sent, and any relevant account or reference numbers that pertain to the consumer.

Reasons for the adverse action

The notice should clearly state the reasons that led to the adverse action being taken. Whether it is issues related to creditworthiness, payment history, employment qualifications, or any other factors considered by the business, these reasons must be explicitly outlined in the notice. Providing a comprehensive explanation helps consumers understand the basis for the decision.

Information on credit reporting agencies

Since credit reports play a significant role in the adverse action process, the FCRA Adverse Action Notice must inform consumers about the credit reporting agencies that provided the information used in the decision-making process. This includes the names, addresses, and contact information of the credit reporting agencies, allowing consumers to reach out and obtain their credit reports if desired.

Consumer’s rights and how to obtain a free credit report

To ensure that consumers are aware of their rights, the FCRA Adverse Action Notice must include a clear explanation of their ability to request a free credit report within 60 days of receiving the notice. This provision enables consumers to review their credit reports and identify any inaccurate or incomplete information that may have contributed to the adverse action.

Contact information for the business

The notice should provide contact information for the business responsible for the adverse action, including the phone number or address that consumers can use to get further information or clarification if needed. This allows consumers to reach out to the business and discuss the adverse action taken against them.

Understanding the Legal Implications of the FCRA Adverse Action Notice

Protection of consumers’ rights

The FCRA Adverse Action Notice plays a vital role in protecting consumers’ rights by ensuring transparency, accountability, and fairness in the decision-making process. It gives consumers an opportunity to understand why the adverse action was taken and address any inaccuracies in their credit reports, ultimately empowering them to take control of their financial situations.

Penalties for non-compliance

Failure to comply with the FCRA Adverse Action Notice requirements can lead to severe consequences for businesses. Regulatory agencies such as the CFPB and FTC have the authority to enforce penalties, which may include fines, litigation, and reputational damage. These penalties aim to deter businesses from neglecting their responsibilities and highlight the importance of adhering to the legal requirements.

Enforcement agencies and their role

The CFPB and FTC are the primary enforcement agencies responsible for overseeing compliance with the FCRA Adverse Action Notice. They work to ensure that businesses adhere to the legal requirements, investigate consumer complaints, and take appropriate action against any violations. These agencies play a crucial role in upholding consumer protection laws and maintaining a fair credit reporting system.

Recent legal developments and case studies

Numerous legal developments and case studies have emphasized the significance of the FCRA Adverse Action Notice and its implications for businesses. Court rulings and settlements have highlighted the importance of accurate, timely, and informative notices, further emphasizing the need for businesses to stay updated on legal developments and best practices relating to adverse actions.

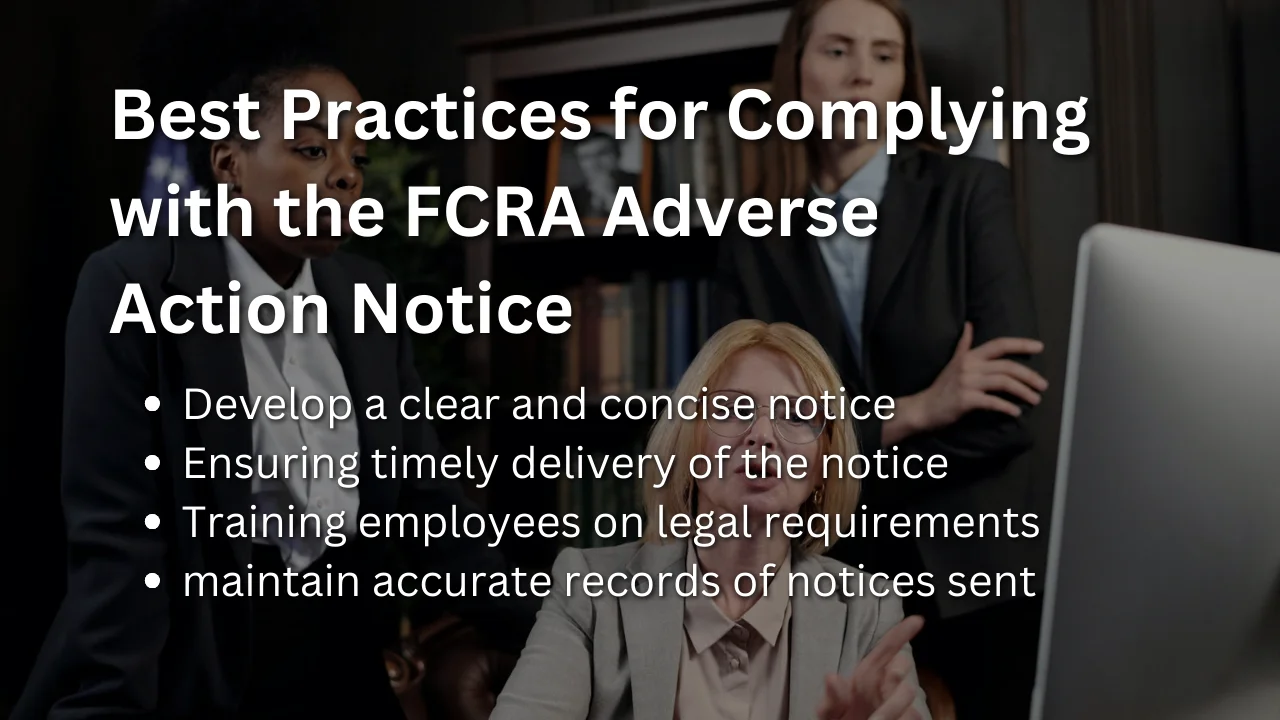

Best Practices for Complying with the FCRA Adverse Action Notice

Developing a clear and concise notice

To ensure compliance with the FCRA, businesses should develop a clear and concise FCRA Adverse Action Notice that includes all required elements. It is essential to use plain language that consumers can easily understand and avoid technical jargon. The notice should be easily readable and free from ambiguity to prevent any confusion.

Ensuring timely delivery of the notice

When an adverse action triggers the requirement for an FCRA Adverse Action Notice, businesses must ensure timely delivery of the notice to the affected consumer. It is crucial to promptly provide the notice within the specified time frame, allowing consumers sufficient time to review their credit reports and exercise their rights if necessary.

Training employees on legal requirements

Businesses should provide comprehensive training to their employees regarding the legal requirements of the FCRA Adverse Action Notice. Employees should understand the criteria that trigger the notice obligation, its content and format, and the importance of timely delivery to consumers. Regular training sessions and updates will help promote effective compliance practices within the organization.

Maintaining accurate records of notices sent

To demonstrate compliance with the FCRA Adverse Action Notice requirements, businesses should maintain accurate records of all notices sent. This includes records of the notice content, the date sent, and the method of delivery. These records can serve as evidence of compliance in the event of an audit or regulatory investigation.

The Role of Credit Reporting Agencies in the FCRA Adverse Action Notice

Responsibilities of credit reporting agencies

Credit reporting agencies play a vital role in the FCRA Adverse Action Notice process. They are responsible for collecting and maintaining consumer credit information, which businesses use to assess creditworthiness and make decisions. These agencies are required to provide accurate and up-to-date information to businesses and promptly investigate and correct any disputed information.

How credit reports are used in the adverse action process

Credit reports serve as the foundational basis for adverse actions, forming the core of the business’s decision-making process. Businesses use credit reports to evaluate a consumer’s creditworthiness, payment history, and overall financial health, among other factors. By analyzing this information, businesses determine whether adverse actions are necessary and justified.

Disputing inaccurate information in credit reports

If consumers believe their credit reports contain inaccurate or incomplete information that led to an adverse action, the FCRA provides them with the right to dispute such information. Consumers can contact both the credit reporting agency and the business that took the adverse action to initiate the dispute process. The agencies are then obligated to conduct a reasonable investigation within a specified timeframe and correct any errors found.

Common Questions and Concerns about the FCRA Adverse Action Notice

What constitutes an ‘adverse action’ under the FCRA?

An adverse action encompasses a broad range of actions taken by a business that negatively impact a consumer’s credit or employment opportunities. It includes decisions such as credit denials, credit limit reductions, changes in terms, and employment denials or terminations based on credit history. Adverse actions can significantly affect a consumer’s financial prospects, and the FCRA Adverse Action Notice ensures transparency in these situations.

Can businesses use a generic adverse action notice?

While a generic adverse action notice may contain some standard information, it is generally not recommended. The FCRA Adverse Action Notice requirements emphasize the need for specific and tailored notices that provide detailed information regarding the consumer’s situation. Using a generic notice may not adequately fulfill the legal obligations and can lead to non-compliance.

How long should businesses retain records of adverse action notices?

Under the FCRA, businesses are required to retain records of adverse action notices for a period of five years. It is essential for businesses to keep accurate records to demonstrate compliance in case of audits, investigations, or legal disputes. Maintaining these records allows businesses to provide evidence of adherence to the FCRA Adverse Action Notice requirements if necessary.

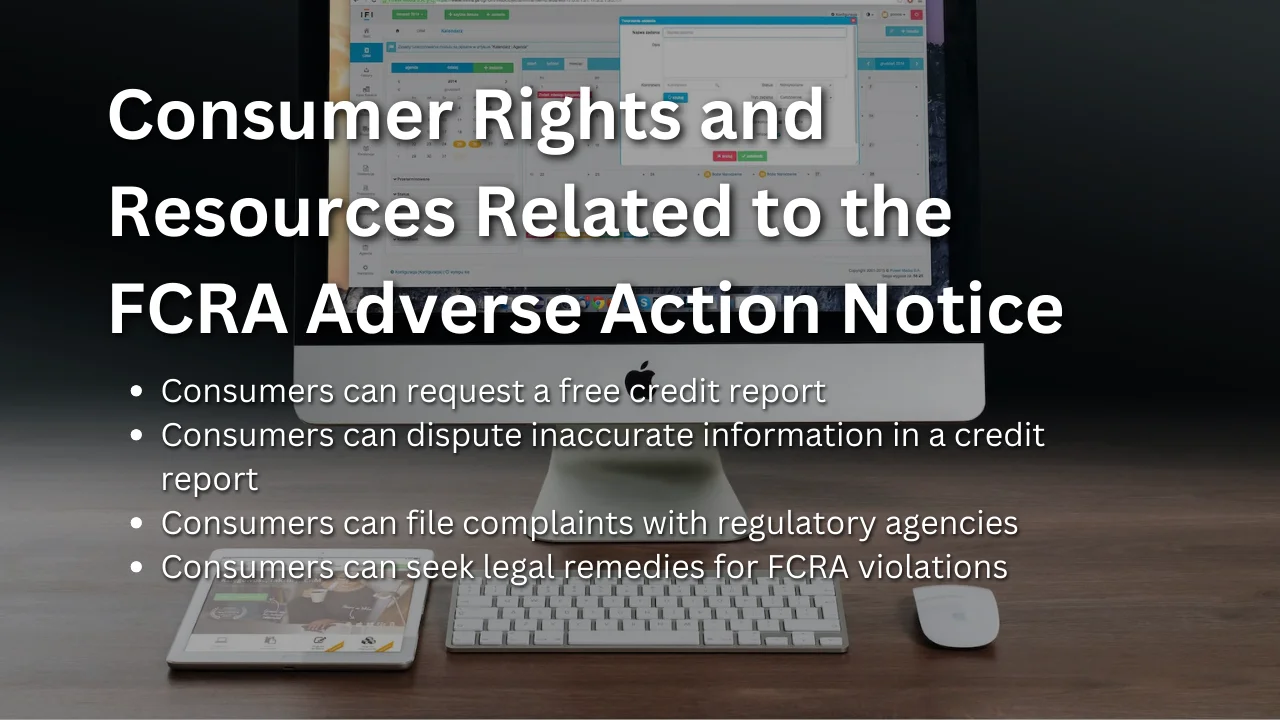

Consumer Rights and Resources Related to the FCRA Adverse Action Notice

How consumers can request a free credit report

Consumers have the right to request a free credit report within 60 days of receiving an FCRA Adverse Action Notice. They can do so by contacting the credit reporting agencies through the provided contact information in the notice. By reviewing their credit reports, consumers can identify any inaccuracies or discrepancies and take appropriate action to rectify them.

Disputing inaccurate information in a credit report

If consumers find inaccurate information in their credit reports that negatively influenced an adverse action, they have the right to dispute such information. They can initiate the dispute process by contacting both the credit reporting agencies and the business responsible for the adverse action. The agencies are then obligated to investigate the disputed information and correct any errors found.

Filing complaints with regulatory agencies

Consumers can file complaints with regulatory agencies such as the CFPB and FTC if they believe their rights under the FCRA Adverse Action Notice have been violated. These agencies have established processes for investigating complaints and taking appropriate action against non-compliant businesses. Filing a complaint helps protect consumer rights and contributes to maintaining fair credit practices.

Seeking legal remedies for FCRA violations

In cases where businesses fail to comply with the FCRA Adverse Action Notice requirements and consumers suffer harm as a result, legal remedies may be pursued. Consumers have the right to seek compensation, including actual damages, statutory damages, and attorney fees, through individual lawsuits. These legal remedies aim to hold non-compliant businesses accountable and provide restitution to affected consumers.

Comparing the FCRA Adverse Action Notice to other Consumer Protection Laws

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA protects consumers from unfair and abusive debt collection practices. While it may be related to adverse actions taken by debt collectors, it differs from the FCRA Adverse Action Notice, which focuses specifically on adverse actions based on credit reports. The FDCPA addresses debt collection practices as a whole and establishes guidelines for communication, disclosure, and harassment prevention.

The Fair Credit Billing Act (FCBA)

The FCBA protects consumers by establishing procedures for resolving billing errors and unauthorized credit card charges. While it is not directly related to adverse actions, it complements the FCRA Adverse Action Notice by providing additional consumer protections when it comes to credit card billing disputes and addressing billing discrepancies.

The Equal Credit Opportunity Act (ECOA)

The ECOA prohibits credit discrimination based on factors such as race, color, religion, national origin, sex, marital status, and age. Although it does not specifically require an adverse action notice, it contributes to the overall framework of fair credit practices by promoting equality and non-discrimination in lending and credit decisions.

Conclusion

The FCRA Adverse Action Notice is a crucial component of the consumer protection framework established by the Fair Credit Reporting Act. By providing transparency, explanations, and opportunities for consumers to correct inaccuracies, the FCRA Adverse Action Notice promotes fairness and accountability in credit-related decisions. Businesses must be well-versed in their obligations under this important legislation and strive to comply with its requirements to protect consumer rights and maintain a reputable image.